Morgan Stanley Predicts Memory Prices Will Peak in Q4 2026

Memory Market Poised for Historic Peak in Q4 2026, According to Morgan Stanley Analysis

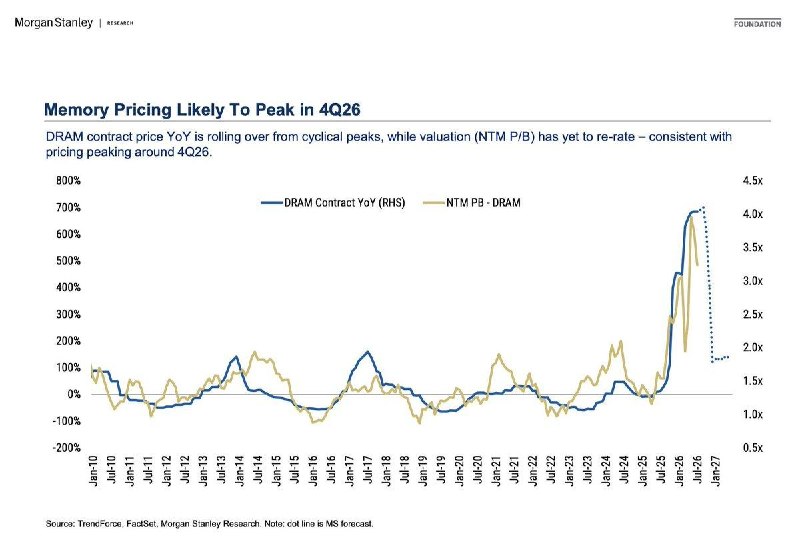

The global memory market, currently experiencing one of its most significant rallies in recent history, is projected to reach a pricing peak in the fourth quarter of 2026, according to a comprehensive analysis by Morgan Stanley. After an unprecedented surge in DRAM (Dynamic Random-Access Memory) prices driven by artificial intelligence demand and constrained supply, the financial institution forecasts a gradual transition from explosive growth to a more normalized pricing environment.

Current Memory Market Dynamics

The memory industry has been undergoing a remarkable transformation, with DRAM contract prices experiencing substantial YoY (year-over-year) growth that has far exceeded market expectations. This surge has been fueled by a confluence of factors, most notably the unprecedented demand from artificial intelligence applications and persistent supply constraints across the manufacturing ecosystem.

"We're witnessing what could be described as a supercycle in the memory market," noted industry analysts. "The combination of AI-driven demand and limited supply capacity has created conditions not seen in over a decade."

The AI Revolution's Impact on Memory Demand

Artificial intelligence has emerged as the single most significant driver of memory demand in recent years. AI applications, particularly large language models and generative AI systems, require exponentially more memory capacity than traditional computing applications. This shift has fundamentally altered demand patterns across the memory landscape.

| Memory Type | Primary AI Applications | Growth Factor (YoY) |

|---|---|---|

| HBM (High Bandwidth Memory) | AI training, high-performance computing | 85-120% |

| Server DRAM | Data centers, cloud infrastructure | 40-60% |

| Consumer DRAM | Standard computing devices | 15-25% |

Strategic Shifts Among Memory Manufacturers

In response to these market dynamics, major memory manufacturers have significantly adjusted their production priorities. Samsung, SK hynix, and Micron—the industry's dominant players—have increasingly allocated their most advanced production capacity to High Bandwidth Memory (HBM) and server-grade DRAM, which command premium pricing and are essential for AI applications.

This strategic reallocation has effectively created a two-tiered market:

- Premium Segment: HBM and server DRAM experiencing strong pricing power and sustained demand

- Standard Segment: Consumer DRAM facing more moderate price increases due to relatively lower demand growth

Supply Chain Constraints and Long-Term Commitments

The memory market's current tightness has been exacerbated by several factors:

- Limited expansion of semiconductor manufacturing capacity

- Extended lead times for new fab construction

- AI giants securing multi-year supply agreements, effectively removing significant volume from the spot market

- Geopolitical factors impacting global supply chains

"Major AI companies are locking in supply for years in advance, which creates a structural shift in how the memory market operates," explained industry experts. "This long-term contracting pattern is unprecedented and contributes to the persistent supply-demand imbalance."

Morgan Stanley's Peak Prediction and Market Transition

According to Morgan Stanley's analysis, the current memory pricing supercycle is likely to reach its zenith in Q4 2026, after which YoY contract price growth is expected to moderate from current cyclical highs. However, the firm emphasizes that this peak doesn't necessarily signal an imminent crash in memory prices.

"We anticipate a transition from explosive growth to a more normalized pricing environment rather than a dramatic correction," stated the Morgan Stanley report. "The fundamental demand drivers from AI remain strong, even as the rate of price increase moderates."

| Time Period | Expected Pricing Trend | Market Conditions |

|---|---|---|

| Now - Q4 2026 | Strong YoY growth | Supply constrained, demand robust |

| Q4 2026 - Q2 2027 | Peak pricing begins to moderate | Gradual supply expansion, demand remains strong |

| Q2 2027 onwards | Normalized pricing environment | Improved supply-demand balance |

Post-Peak Market Outlook

Even after the anticipated peak in late 2026, memory shortages are likely to persist into 2027 due to the significant time required to bring new manufacturing capacity online. Semiconductor fabrication facilities (fabs) typically require 2-3 years from planning to full production capacity, creating a lag between market signals and actual supply increases.

The memory industry is also facing technological challenges as it scales to meet AI demands. The transition to more advanced memory technologies, including next-generation HBM and DDR5/DDR6, requires substantial R&D investment and manufacturing process refinement, further extending the timeline for significant capacity expansion.

Industry Leaders and Strategic Positions

As the memory market evolves, three major manufacturers continue to dominate the landscape:

| Manufacturer | Market Position | Strategic Focus | Technological Advantages |

|---|---|---|---|

| Samsung | Market leader in DRAM and NAND | HBM leadership, vertical integration | Most advanced process nodes, HBM3E production |

| SK hynix | Strong in HBM and mobile memory | HBM specialization, AI partnerships | HBM technology leader, advanced packaging |

| Micron | Third in DRAM, strong in NAND | Cost competitiveness, US manufacturing | 1-beta technology, high-capacity modules |

Implications for Various Sectors

The evolving memory market will have significant implications across multiple sectors:

- Data Centers: Will continue to prioritize memory capacity and performance, potentially passing some costs to end users

- Consumer Electronics: May face component constraints as manufacturers compete for limited supply

- AI Startups: Will need to factor in memory costs as a significant portion of their infrastructure expenses

- Cloud Providers: Will accelerate in-house memory development to reduce dependency on external suppliers

Conclusion: Navigating the New Memory Landscape

The memory market is entering a period of unprecedented transformation, driven by AI demand and constrained supply. While Morgan Stanley's prediction of a Q4 2026 peak suggests moderation in the rate of price increases, the underlying fundamentals point to a market that will remain structurally different from pre-AI era dynamics.

"The memory industry is at an inflection point," concluded industry analysts. "What we're witnessing isn't just a cyclical upturn but a fundamental reordering of the memory market that will have lasting implications for technology development across virtually every sector."

As Samsung, SK hynix, and Micron navigate this evolving landscape, their strategic decisions regarding capacity allocation, technology development, and customer partnerships will shape not only their own futures but the trajectory of the entire technology ecosystem for years to come.

Memory prices could PEAK in Q4 2026, says Morgan Stanley 📈 After one of the biggest DRAM rallies in years, Morgan Stanley believes memory pricing is likely to top out around Q4 2026, with YoY contract price growth expected to cool from current cyclical highs. Key takeaways: • DRAM prices have surged due to the AI boom and tight supply. • Memory makers are prioritizing HBM and server DRAM over consumer chips. • AI giants continue locking in long-term supply, keeping the market tight. • Even if pricing peaks in late 2026, shortages could remain into 2027 as new capacity takes years to come online. This doesn't necessarily mean memory prices will crash overnight. It suggests the market could transition from explosive growth to a more normalized pricing environment after an unprecedented AI-driven supercycle. Samsung, SK hynix and Micron remain the biggest companies to watch. 🚀📉 ❤️ @techroma Memory prices could PEAK in Q4 2026, says Morgan Stanley 📈 After one of the biggest DRAM rallies in years, Morgan Stanley believes memory pricing is likely to top out around Q4 2026, with YoY contract price growth expected to cool from current cyclical highs. Key takeaways: • DRAM prices have surged due to the AI boom and tight supply. • Memory makers are prioritizing HBM and server DRAM over consumer chips. • AI giants continue locking in long-term supply, keeping the market tight. • Even if pricing peaks in late 2026, shortages could remain into 2027 as new capacity takes years to come online. This doesn't necessarily mean memory prices will crash overnight. It suggests the market could transition from explosive growth to a more normalized pricing environment after an unprecedented AI-driven supercycle. Samsung, SK hynix and Micron remain the biggest companies to watch. 🚀📉 ❤️ @techroma